How AI & ML Can Streamline Financial Compliance and Risk Mitigation

Managing risk and regulatory compliance in today’s connected and digital world is becoming increasingly complex and expensive. As a result, artificial intelligence (AI) and machine learning (ML) have gained popularity in the last decade to increase efficiency productivity and reduce costs across industries.

As traditional banks compete relentlessly with new fintech companies, their legacy software and infrastructure need an upgrade. Moreover, the digital revolution has also given rise to new tech-savvy customers who want more from banks.

Artificial intelligence and machine learning have thus opened new doors for financial compliance and risk mitigation. Check what they are!

How AI & ML Can Streamline Financial Compliance and Risk Mitigation

Since financial institutions handle sensitive data daily, they are naturally prone to risk. Artificial intelligence is the most efficient way to manage those risks in a growing and competitive industry.

As a result, we are witnessing the dawn of a new era in risk management with the help of AI and ML. See how AI & ML can mitigate the inherent risks associated with banking and finance:

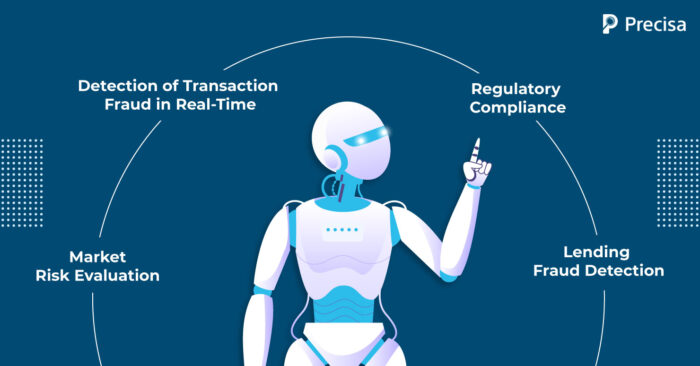

1. Real-time transaction fraud detection

Financial fraud constitutes a tiny fraction of all transactions, but it is a primary concern for banks and every industry that relies on digital payments. A total of 1.38 trillion rupees was lost to banking fraud in India in 2021.

More people are making purchases digitally than ever before, adding to the problem, as fraudsters have more attack surfaces to exploit with post-pandemic situations. At the same time, the cost of cyberattacks is on the rise.

Banks have traditionally used fraud detection models designed for physical credit cards and structured around rules based on historical analysis of incidents.

Unfortunately, rule-based systems are insufficient for today’s online purchases to keep up with modern commerce or the increasingly complex payment fraud schemes criminals perpetrate.

A more sophisticated approach is needed here: machine learning and AI. As more and more data is processed, these systems constantly adapt to the new rules and provide security from various risks and fraud.

The task uses two machine learning algorithms: supervised and unsupervised.

- Supervised learning identifies fraud patterns by using annotated historical data.

- Unsupervised learning involves using unlabelled datasets and analysing relationships that human investigators may not notice.

Both approaches combine to analyse transaction flows holistically, identify patterns in user behaviour, detect fraudulent activity in real-time and remove it from the system.

2. Regulatory compliance

As banks are exposed to different risks, compliance with federal and international regulations helps them reduce those risks. However, keeping up with regulations is expensive.

The advantages of machine learning over humans for this task are that they can quickly process vast amounts of data and identify correlations we would not have noticed otherwise.

ML solutions can also improve compliance systems by reducing, if not eliminating, the number of false-positive alerts. Currently, each of these alarms triggers a compliance officer to review it.

But sooner, the ML algorithms can streamline operations reduce costs and fraud by only raising alarms when human expertise is needed. The tech works based on the data collected by compliance officers over a period and understanding the compliance fraud patterns.

3. Market-risk evaluation

In market trading, artificial intelligence is a perfect tool to reduce risk to the maximum. For example, it can take a human at least several days to review vast quantities of data points, but machine learning algorithms can examine vast volumes of data points in just a few seconds.

These insights provide traders with optimal price points (about the risk of losses), allowing them to make more accurate forecasts in the future. As a result, trading firms minimise trading risk while achieving greater returns.

Again, trading technologies is a good example here. The firm combines machine learning with powerful processors to identify trading patterns across multiple markets.

4. Lending fraud detection

The internet has magnified the prevalence of lending fraud—a long-standing problem for financial institutions. Today, fraudsters can easily create and use fake IDs, mobile phone numbers, and social security numbers to obtain illicit benefits.

Lenders are in a bind because consumers and businesses require loans promptly; on the other hand, rigorous loan assessments can take a long time, and fraudulent applications should be detected and thwarted early.

However, traditional rule-based systems examining past user behaviour and historical data have difficulty seeing complex fraud schemes of the modern world.

This scrutiny should include synthetic identity fraud created by combining real and fake information, loan stacking-applying for multiple loans simultaneously, and account takeover, where a fraudster takes over a consumer’s account.

Furthermore, machine learning algorithms aren’t limited to a limited number of variables; they can detect anomalies, irregularities, and odd patterns with better accuracy and speed.

In addition to cross-referencing applications, machine learning can uncover pertinent information. Models get “smarter” the more datasets they examine, as past learnings can also be applied to future applications.

5. Reduce human-errors

Besides, AI and ML in the financial sector can also help eliminate human errors. Regulatory industries spend billions of dollars each year on human error. In addition, as per IBM’s study, human error accounts for 95% of all cyber security breaches.

Financial management is prone to human error for many reasons – inefficient processes, outdated technology, or negligence, to name a few. Information overload also presents several opportunities for confusion, leading to human error.

In today’s increasingly technology-driven regulatory compliance landscape, applications that use AI and ML can help mitigate the adverse effects of human error.

Finally, financial compliance and risk mitigation issues are primarily data issues. The key is to establish a robust data strategy that can analyse voluminous numbers of data, manage model risk transparently, and leverage real-time insights. That helps financial institutions and fintechs to level up future-proof compliance teams.

Need AI-based solutions to meet your lending needs? Are you interested in knowing more about such information? Then, get in touch with Precisa. We deliver an agile bank statement analysis tool that makes financial compliance and risk mitigation a breeze. How does Precisa work?

The Bank Statement Analyser gathers data from bank statements, classifies and categorises transactions, analyses the data, finds fraudulent transactions and other irregularities, and assigns a Precisa score to overall creditworthiness.