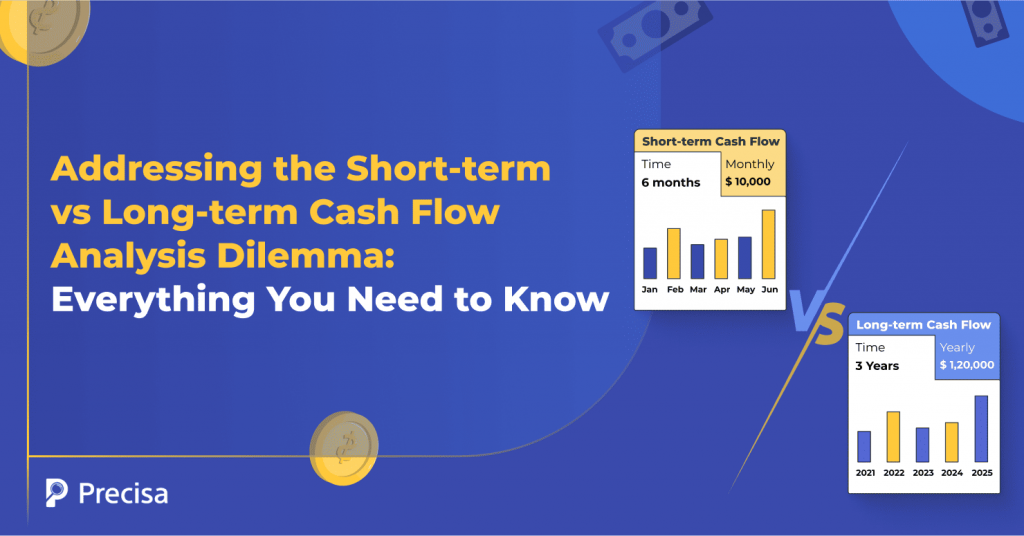

Delinquencies in India increased by 44% among personal loan borrowers between Dec ’23 and June ’24. This highlights the importance of accurate and informed decision-making during loan approvals and, more importantly, the need to rethink how lenders approach cash flow analysis of individual and commercial borrowers. Although conventional lenders in India, including banks, typically rely […]