Top 5 Fintech Trends Transforming the Digital Lending Landscape

In the post-pandemic world, the Fintech business, like any other, is experiencing changes and facing its own set of unique challenges. FinTech adoption doubled every two years, increasing from 16 per cent in 2015 to 64 per cent in 2019 (Fincom Alliance).

The increasing need for digital transformation in companies of all sizes led to the rapid surge of digitisation. Fintech trends have evolved in response to customer expectations. The FinTech landscape is almost unrecognisable compared to a year ago.

Fintech Trends in Banking and Financial Services

Fintech is positioned to develop and evolve continually. Digital payments, automated underwriting, open banking, peer-to-peer lending, mobile banking, and digital identification are just a few examples of business models that have been around for a decade.

These transformations led to increased customer satisfaction, a reduction in cost, and the creation of alternative product options based on customers’ needs. The digital lending business is undergoing a similar transformation right now and has advanced significantly over the past decade.

Bright and Promising Future of Digital Lending

The necessity to overcome the conventional ‘pain points’ (time-consuming, extensive, complicated, manual) in the lending process prompted the digitisation of lending. Paperless and faster lending processes have been made possible by digitisation.

Digital lending is emerging to be a powerful tool for connecting with people previously unable to access financial services. Due to differences in market structures, regulatory contexts, and customer needs, a diverse range of digital lending models have emerged, each addressing financial inclusion in a unique way.

Fintech Trends: How Fintech is Helping the Lending Industry

The Fintech industry is expanding out into the digital realm. The banking and financial sector has benefited greatly from technological innovations, particularly in the area of digital lending. Lenders now have new ways to market their services to the general public.

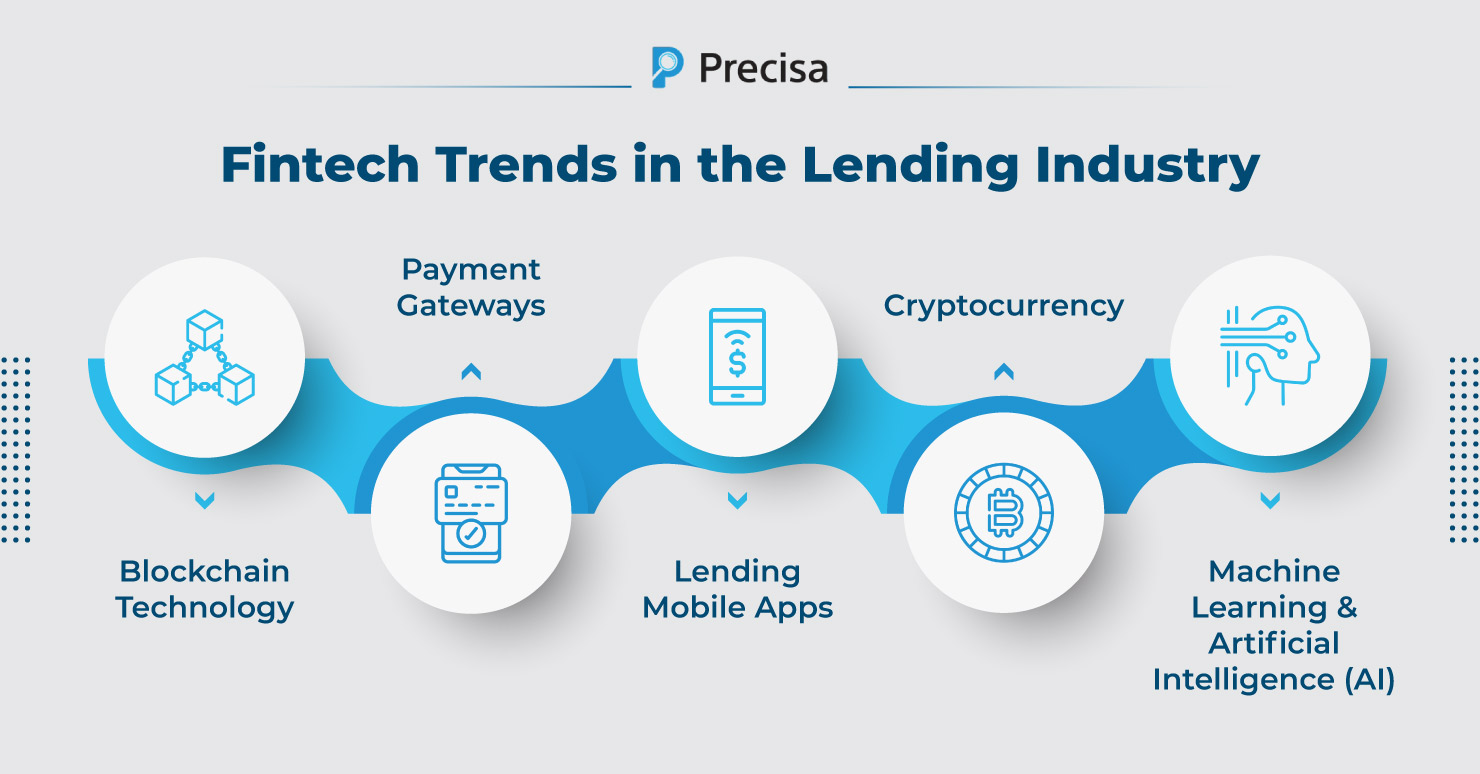

Here are five Fintech trends that transformed the digital lending sector. This transformation shows how huge the impact of FinTech is in the lending industry.

1. Blockchain Technology

In the financial business, blockchain is one of the most extensively deployed technologies. It assists in resolving the issues that most customers face, particularly in the lending sector. With the pressures of new technologies and increasing consumer expectations, traditional lending has become outmoded and is slowly breaking down.

A look into the banking sector’s adoption of Blockchain technology in India demonstrates that there is strong momentum in favour of the technology. A group of prominent Indian banks has created a partnership to collaborate on Blockchain initiatives. At this time, 11 Indian banks have joined a consortium to develop and implement a blockchain-based credit system for India’s small and medium businesses (SMEs). ICICI Bank, Axis Bank, HDFC, Yes Bank, Standard Chartered, Kotak Mahindra, South Indian Bank, and RBL are among the banks in the partnership (Money Control).

The Maharashtra State Warehousing Corporation (MSWC) has launched a pilot program to leverage blockchain technology to enable farmers to obtain commodity finance more quickly. Farmers can now get loans against their commodities in 24 hours, rather than the standard seven days, thanks to blockchain technology (DNA).

Digital lending firms can develop a low-cost, high-trust platform using blockchain technology. With online loan processing, consumers can keep a record of transactions/documents on an ‘anonymous digital ledger platform’, eliminating the necessity for intermediaries/third parties.

2. Payment Gateways

Payment Gateways are the most popular new payment option today. It is a simple and secure money transfer platform that you can use anytime and anywhere, using your computer or mobile phone. You can select from different options that are available on the market.

Payment gateways have made the digital transformation of lending possible. While the first “online” loan application surfaced in 1985, it was not until the rise of Amazon Pay, PayPal, Stripe, and other similar services that credit became totally digital and readily available.

The overall transaction value in alternative lending is expected to reach over USD 378 million by 2025 with an annual growth rate of 4.43% (Statista). This indicates that the alternative lending sector will surpass all previous records in terms of annual growth rate. Any lender’s goal is to give users appropriate and flexible payment ways — primarily digital — in order to beat out the increasing competition.

According to Statista, the total transaction value in the digital payments segment is expected to surpass USD 6.76 million in 2021 and reach USD 10.72 million by 2025, representing a 12.24% annual growth rate (Statista). Borrowers are more likely to utilise digital and mobile wallets (over 40%) than bank transfers, debit cards when it comes to digital transactions globally.

3. Lending Mobile Apps

Loan lending apps, like most other apps that have simplified a lot of things for us, have come to the rescue of individuals looking for loans.

You can get access to a variety of loan apps with a few taps on your mobile phone, all of which offer speedy application approval and cash release. Consumers are only required to submit a few documents, such as valid identification and a filled form given by the lenders.

Mobile finance is booming, and new companies are being established all the time. From September 2019 to August 2020, over 4.3 billion fintech apps were downloaded (CBInsights), and the numbers are only expected to rise as banks speed their digital transformations and more FinTech businesses enter the market.

According to a recent study, mobile banking apps are in third place among the most utilised apps (Citibank). In 2020, digital banking witnessed significant consumer adoption, and financial services companies throughout the world are reevaluating their tech infrastructures and evaluating the best solutions to meet their customers’ expanding digital demands.

4. Cryptocurrency

Crypto financing has only recently begun to gain traction. Cryptocurrency is a type of digital currency which you can buy and sell. In short, it is a digital or virtual currency that is secure and safe, thanks to cryptography. Cryptocurrency finance or lending is a form of alternative lending in which lenders lend money to borrowers using cryptocurrency in exchange for a fee.

A cryptocurrency-backed loan, like a securities-based loan, uses digital currency as security. The fundamental principle is similar to that of an auto loan or mortgage: you pledge the crypto assets in exchange for a loan, which you then repay over time.

According to PointPay, the market for crypto loans, in which bitcoin and stable coins are pledged as collateral, is predicted to be worth USD 30-35 billion in 2021, and it is expected to continue to rise (The Guardian)

Over the previous several years, the Indian cryptocurrency market has grown at an exponential rate, and it is expected to reach USD 241 million in India by 2030 and USD 2.3 billion globally by 2026 (Mint).

Crypto lending and borrowing have gained traction in India, signalling the dawn of a new financial era. With 450000 retail customers, centralised crypto lending platforms like BlockFi has established a firm foundation.

5. Machine Learning and Artificial Intelligence (AI)

Fintech is based on machine learning and artificial intelligence and adopting machine learning and AI into more segments as they progress. AI and machine learning technologies, which were formerly thought to be nascent, are now at the forefront of financial services, particularly lending.

These technologies are being used by lenders to automate difficult processes. The majority of this is back-end work. Machine learning and AI can help detect frauds, automate loan offer generation, and credit scoring.

Precisa provides high-value research and tech-based solutions to help meet banks’ lending goals. With the help of a complete suite of AI-integrated technology, they provide speedier, uncomplicated, and cost-effective lending solutions.

Precisa is an online bank statement analysis tool used by lending institutions to process and analyse bank statements of prospective loan applicants. The tool has several built-in security checks, as well as a Precisa Score, which calculates the likelihood of loan repayment, as well as other data indicators.

Takeaway

Fintech is still in its infancy, and more innovations are on the way. While the Fintech ecosystem has seen rapid growth over the last few years, it has enabled the creation of digital lending services. This has revolutionised loan procurement and disbursement procedures.

As technology continues to evolve, it is expected that Fintech will evolve along with it. In light of the present situation of Fintech businesses, banks must respond to Fintech trends in a better way to evolve and grow.

Precisa’s BSA can process over 15000 transactions in as little as 6 minutes. It can give a reliable and timely report on an applicant’s creditworthiness, allowing banks to make more informed decisions.

Hence, assessing the creditworthiness of borrowers with Precisa’s bank statement analysis tool becomes simple and cost-effective. So, get started with Precisa and reap the benefits of the 14-day free trial!